Executive Summary

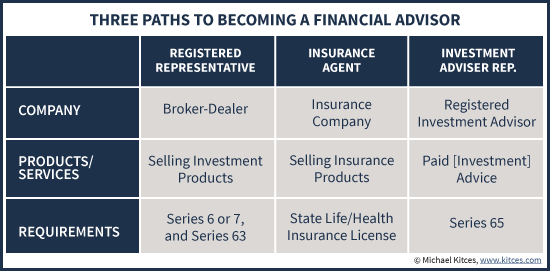

Virtually all financial advisors today follow one of three paths in becoming a financial advisor – either as a registered representative of a broker-dealer, an insurance agent with an insurance company, or an investment adviser representative of an RIA. And each path has its own licensing and exam requirements.

Yet the sad commonality of all paths to becoming a financial advisor is that the actual exam and educational requirements to be an advisor are remarkably low. In fact, the licensing exams for financial advisors do little more than test basic product knowledge and awareness of the applicable state and Federal laws, and none require any substantive education in financial planning itself before holding out to the public as a comprehensive financial advisor who will guide consumers about how to manage their life savings!

Given the roots of financial advising in the world of insurance and investment product sales, this isn’t entirely surprising. The licensing requirements to become a financial advisor, along with the suitability standard to which most advisors are subject, are built around the concept that “advisors” are really just product salespeople. And the bar to determine if someone is "capable" of selling a product isn't very high.

Ultimately, though, if financial advisors hope to actually be recognized as bona fide professionals, the requirements to become a financial advisor must become harder, and require actual education and experience to demonstrate competency as a financial advisor (not just compliance with the laws that apply to salespeople!). Otherwise, the reality is that even if a uniform fiduciary standard is implemented that requires all brokers and investment advisers to act in the best interests of their clients, consumers may still be harmed by advisor ignorance and the sheer lack of competency that would result from raising the fiduciary duty of loyalty but ignoring the equally important fiduciary duty of care – to only give advice in areas in which the professional is actually educated and trained to give advice in the first place!

Financial Advisor License Requirements - How To Become A "Financial Advisor"

Notwithstanding the popularity of the “financial advisor” job – now up to #25 on the list of “100 Best Jobs” from US News, with a projected jobs growth rate of 27% through 2022 from the Department of Labor – the reality is that the term “financial advisor” itself is largely unregulated. The requirements to become a financial advisor are not dictated by whether the person holds out to the public as a financial advisor, and there is no such thing as a standalone "financial advisor license". Instead, licensing requirements for financial advisors are based on the products that the financial advisor provides and how the financial advisor will be compensated for his/her services.

Registered Representative With A Broker-Dealer

For instance, to become a financial advisor who will implement investment (“securities”) products for a commission, you must complete FINRA registration and take certain exams. Most commonly, this will be the 2-hour Series 6 (for selling ‘packaged’ investment products like mutual funds or variable annuities) or the more comprehensive 6-hour Series 7 (for selling everything a Series 6 covers, plus almost any other securities-related product including direct stocks, bonds, options, and more), along with a 75-minute Series 63 (in most states) to affirm the individual understands applicable state securities laws as well. The exams require a passing grade of 72% (or only 70% in the case of the Series 6).

The process is generally accomplished by engaging initially with a broker-dealer, which will sponsor the individual to take the Series exams, after which the person becomes formally registered with FINRA (the regulator) and subsequently becomes a “registered representative” of the broker-dealer (who will oversee their sales activity, in exchange for keeping a portion of the income [commissions] earned).

Insurance Agent With An Insurance Company

By contrast, becoming a financial advisor who will sell/implement insurance products, from life or disability insurance to health insurance or long-term care insurance, must obtain a state insurance license. The exact requirements for these exams vary by state, but generally require some pre-education to learn the basics of insurance products and state insurance regulations, followed by a 1-2 hour exam, again typically with a required passing grade around 70%.

Once completed, the advisor then becomes appointed with one or several insurance companies to be legally able to act as the insurance company’s agent and sell its insurance products to consumers.

Investment Adviser Representative (IAR) with a Registered Investment Adviser (RIA)

The third primary path to become a qualified financial advisor is to give financial advice and get paid for it directly, i.e. by getting paid an advice or investment management fee (rather than a commission tied to an investment or insurance product).

Technically, advisors who wish to get paid a fee for their general advice can do so without being registered or regulated at all in most states; however, if the advice pertains to specific investment advice for which the advisor is compensated, it’s necessary to become registered as an investment adviser in any state(s) where the advisor has client(s). Ultimately, being so registered requires creating a business entity (or formally registering as a sole proprietor business) that will be the “Registered Investment Adviser” (RIA) entity with the state, and the individual becomes an investment adviser representative (IAR) of that company. Alternatively, a financial advisor might choose to work for an existing RIA (either registered in the state, or registered nationally with the SEC [for larger RIA firms]), becoming an IAR of that existing firm instead.

Becoming an IAR of an RIA (whether a new or existing RIA) requires the prospective advisor to complete a 3-hour Series 65 exam, which covers the state laws pertaining to getting paid for investment advice, and similar to other FINRA Series exams has a 72% required grade to pass.

Notably, in many states, any advisor who has CFP certification is automatically presumed to be delivering specific investment advice for a fee, and thus must become an IAR of some RIA registered in that state; however, many/most of those states also waive the Series 65 exam for CFP certificants, which means the advisor must simply go through the paperwork registration process (and pay the state registration fee) with the state securities department (but won’t necessarily have to take any licensing exams).

Financial Advisor Competency Standards For Advice Versus Product Sales

A notable commonality of all the current regulatory paths towards becoming a licensed financial advisor is that in the end, the actual regulatory exams focus on the basic structure and mechanics of the products being used (e.g., the Series 6 covers how mutual funds work, the Series 7 covers how stocks/bonds/options work, the life & health insurance license covers how those insurance products work). And the regulatory exams are also meant to ensure that the advisor understands the basic laws that will apply to him/her as an advisor. Notably absent from the licensing requirements for becoming a financial advisor, though, is any kind of test to determine if the “advisor” actually knows anything about money, finances, or advice!

In other words, the sad reality is that meeting the legal registration/licensing requirements to become a financial advisor is simply about understanding the relevant laws and products, and never actually involves demonstrating any competency in financial advice itself. Educational programs in financial planning and advice, and certifications like the CFP marks (or post-CFP educational programs beyond that), are purely optional, and while they are viewed as a “best practice” for advisors to have, the only actual requirement is a fairly minimal licensing exam. Which means there's actually no such thing as a certified financial advisor (just a licensed financial advisor who has voluntarily completed the Certified Financial Planner designation), and you can technically become a financial advisor with no experience at all!

By contrast, even becoming a hairdresser requires in most states the completion of a 9-month educational program in hairstyling for either a cosmetology certificate or an associate’s degree… which is 9 months more in educational requirements than it takes to become a financial advisor and provide consumers guidance about their entire life savings!

Given that the roots of becoming a financial advisor are in the sale of insurance or investment products, these regulatory standards are not entirely surprising. Because the fundamental difference in even a trade like hairstyling versus selling insurance or investment products is that one is an actual service with standards to which a professional can be held accountable, while the other is “just” the job of a salesperson selling products (in a world where 'caveat emptor' reins supreme!).

Accordingly, the only legal requirements to become a financial advisor are to get registered for the sale of products (and understand the laws that apply to such products), and the only “standard” of accountability for those financial advisors with their clients is the “suitability” standard (a legal standard for salespeople that requires them not to push products that are completely unsuitable for the recipient), not an actual advice-based fiduciary standard that requires advice to be delivered in the best interests of the client.

Sadly, though, it’s also worth noting that the standard for investment advice as an RIA – which is an advice-centric fiduciary standard – is actually still remarkably low as well, at least in the context of minimum requirements today. While the courts (or an arbitration panel) may sanction an investment adviser representative for failing to meet the standard of a prudent expert when working with clients, there’s still no actual requirement for the advisor to demonstrate in advance that he/she is capable of meeting such a competency standard; instead, advisors are turned loose on the public, and consumers can only seek legal recourse after the fact to recover any damages that result from a bad advisor’s incompetence. And, even the prudent man standard is still built primarily around prudent investment strategies, not all of the other areas in which a comprehensive financial advisor might provide financial advice. In other words, there's no clear accountability standard for advice when it comes to bad cash flow, budgeting, retirement, insurance, or income tax or estate planning advice!

Raising Educational Requirements To Become A Financial Advisor, And The Fiduciary Duty Of Care

Ultimately, if financial advice hopes to emerge as a bona fide and recognized profession, the standards for becoming a financial advisor in the first place need to be raised. A consumer-centric financial advice profession cannot be managed to a product-sales-based standard, with educational requirements significantly below even trades like cosmetology.

Notably, the issue of lifting the standards of advice has already been an ongoing issue of recent regulatory debate, from the potential for a uniform fiduciary standard for brokers and investment advisers, to the ongoing revisions to the Department of Labor’s proposals to expand the fiduciary standard by requiring even salespeople to sign a “best interests contract” with clients or risk that their commission-based compensation will be treated as a prohibited transaction.

The caveat to the current fiduciary debate, however, is that it is primarily about the duty of loyalty, and the idea that a bona fide advice professional should be required to give advice that is in the best interests of the client. While that is certainly one aspect of fiduciary advice – and an important one – it is not the only one. The other key to fiduciary duty is that even if advice is delivered solely in the interests of consumers, if there is no process to ensure the people delivering the advice are competent in the first place, consumers will simply be harmed out of [advisor] ignorance rather than greed or malice.

In other words, enforcing a fiduciary duty of loyalty on advisors - a "best interests standard" - without lifting the standard for the corresponding fiduciary duty of care, simply means that consumers will be harmed by the [well-intentioned-but-uneducated] advisor’s sheer incompetency, rather than his/her inability to manage conflicts of interest. In fact, given that most advisors are good and honest people and try to act in their clients’ best interests – regardless of whether they’re subject to a fiduciary standard that legally requires it – it’s likely the case that even now, most of the consumer harms caused by salespeople posing as financial advisors are due to a lack of training and education, not a deliberate attempt to take advantage of clients. And while most financial advisors are required to acknowledge at least some limitations to their scope of care and competency – e.g., disclosures from advisors that their ‘advice’ does not constitute formal tax or legal advice – even within the broad realm of financial advice, advisors commonly give “advice” far beyond the scope of their actual education and training (especially given that no advice-related education is required at all!). Though in a fiduciary future, failing to limit the scope of advice that goes beyond an advisor's competency could expose them to legal liability.

Financial Planning As A Recognized Profession

The bottom line is that most bona fide professions (e.g., doctors, lawyers, etc.) have not only a fiduciary duty to act in the interests of their clients, they also have substantive competency requirements to become a professional in the first place, including both extensive (graduate-level) educational requirements and what is often an experience or outright ‘apprenticeship’ (e.g., residency) requirement as well.

By contrast, financial advisors still only must take a minimum regulatory exam about the laws that apply to selling products, with no experience requirement, and no educational requirements regarding financial advice itself. At best, our educational standards – like earning the CFP certification – are purely voluntary, and sadly even the CFP marks have been trending recently towards a lower experience requirement, not a higher one.

Which means in the long run, even the fiduciary battle now being waged about acting in the best interests of clients is victorious, it will really just be one step in the ongoing process of lifting the standards for financial advice. The duty of loyalty may be the battleground today, but the duty of care and a competency standard for financial advisors won't be far behind, as it is essential for truly protecting the public. After all, financial planning is sacred work to clients – as is the work of any bona fide profession – which means in the long run, the requirements for becoming a financial advisors should be reasonably stringent and challenging, in terms of both managing conflicts of interest for the client's benefit, and having the professional competency to give the advice, too!

So what do you think? Are the requirements to become a financial advisor too easy in today's environment? Should the educational and experience requirements be lifted, along with other proposed fiduciary reforms? Should financial advisors actually be tested for their financial knowledge before being allowed to receive financial licenses for giving financial advice to the public?

All I can say is that I’m sick of apologizing for the industry.

Have to disagree with you (which is unusual!). Making it more difficult to become an advisor will eventually serve to drive up costs for the consumers we are trying to “protect.”

To use the example you referenced above, the licensing or stricter licensing of professions such as hairdressers creates benefits mainly for those within the profession, because it essentially creates a de facto cartel and drives up prices (wages). The problem isn’t that financial professionals need more licensing, the problem is that someone thought it was a good idea to require a license to cut hair!

While there can be benefits of stricter licensing, I think those benefits are largely outweighed by the additional costs to consumers. See this paper for more on higher costs imposed by over-licensing: http://isps.yale.edu/news/blog/2013/11/is-the-us-%E2%80%9Cover-licensed%E2%80%9D-the-case-for-reforming-america%E2%80%99s-professional-licensing#.Vds-sPlVhBc

The better middle ground solution is probably something like the CFP board, which is a voluntary standard, but rigorous enough to set apart advisors who are serious about their craft and about serving their clients with excellence.

There are some that find the CFP too easy to obtain as well…I’m not sure this will ever have a single solution, because the bar will just keep changing.

Yet, I do think additional requirements should be added. Working in both the Insurance/BD and RIA world, I’ve seen a lack of basic financial knowledge by many “advisors.” It’s pretty concerning.

Will “over-licensing” change it? Not sure…

Last thing on cost. While it may drive up the costs…I think consumers would just go another direction for their advice, therefore bringing the demand down and then the cost.

I couldn’t agree with you more, Aaron. During my 45 year career, I had the insurance licenses, Series 3 (futures and options), Series 6 (mutual funds and variable products), series 7 (stock broker), RIA, and became a Certified Commodities Trading Adviser trading discretionary accounts. The latter was the only one that required disclosure of actual performance history. It took self-study and experience to learn how to read market behavior, and probabilities of markets through technical analysis. None of the study materials for any of these licenses teach any of that.

Most “experts” aren’t much more accurate than a blind monkey with a dart. Anyone who had his clients over-weight stocks going into the current market decline should have his license revoked.

Here, here, Aaron. The regulatory requirements of hairstylists should not used as a standard. I realize Michael was using it to provide a frame of reference, but I think the legal or medical field would have been a better relative standard.

Another consequence of regulatory requirements would be the perception of competence when working with an advisor who has gone through the process of stricter licensing, which could lead to consumers diminishing or neglecting their responsibility to properly vet where their financial advice is coming from.

However, this perception exists now, which is why I believe Michael’s point is a good one. So…what if we DEregulated from where we currently sit in financial products and services? Sounds crazy (and can’t imagine it ever happening) but what would be the consequences? I think it would create more space for private industry standards and certifications that would be much more effective at protecting consumers than state requirements.

Along those lines, if the CFP experience and competency requirements become less stringent, won’t that create an incentive for a more strict certification to arise. I would certainly consider striving for the highest level of certification in financial advice for differentiation.

Aaron,

Actually, higher standards do not always drive up costs. In markets with significant information asymmetry, higher standards bring DOWN costs by ensuring that quality providers can succeed and that low-quality providers are weeded out (because with high informational asymmetry, markets are not capable of weeding out bad players effectively on their own). This is WHY all bona fide professions have established higher barriers to entry (and why it’s good for consumers that they have).

See Akerlof’s “The Market For Lemons” research on standards in situations of asymmetric information – https://en.wikipedia.org/wiki/The_Market_for_Lemons – work for which he ultimately won the Nobel Prize in recognizing that when consumers can’t properly vet quality, the BAD can actually drive out the GOOD. :/

– Michael

Your application of “The Market for Lemons” fails on several accounts. Let’s examine the five criteria for a lemon market (spelled out in the Wikipedia article you linked):

1. “Asymmetry of information, in which no buyers can accurately assess the value of a product through examination before sale is made and all sellers can more accurately assess the value of a product prior to sale”

This assumption (sort of) works in car markets, because cars have no way of signalling their value to potential buyers. However, these dynamics are entirely different in the financial advisor market. A much better use of economic theory to approach this transaction with asymmetric information would be Michael Spence’s job-market signalling model.

Spence assumes that when an employer is evaluating an applicant, there are two general categories of observable attributes — indices and signals. Attributes that cannot be manipulated by an applicant are indices and attributes that can be manipulated are signals. If employers could only rely on indices, then the problem of asymmetric information could not be overcome. However, because good employees have a strong incentive to differentiate themselves from bad employees, they also have a strong incentive to invest in signals. Spence specifically focuses on the signal of education and its value as a “credential”.

Take two financial advisors with equivalent indices. Even if the CFP provided no productive value, it can provide value as a signal because, all else equal, the opportunity cost (both time and money) of acquiring the credential will be lower for the “better” advisor (this does assume that education and quality of advice are correlated). The result will be that “good” advisors invest in more education than “bad” advisors — narrowing the information gap and giving consumers a reliable metric to evaluate advisors on. The CFP is simply one of many signals advisors have at their disposal (including other forms of education, industry involvement, demonstrated client service, “free” advice, etc.). Additionally, consumers can use their own metrics (interview questions, referrals, etc.) to vet advisors in a way that cannot be done with cars.

Long story short, consumers do have reliable metrics to evaluate advisors on, if they choose to use them (which is fundamentally at odds with the assumptions of “The Market for Lemons”). These metrics may not be perfect, but they need not be in order for the benefits of signalling to manifest.

2. “An incentive exists for the seller to pass off a low-quality product as a higher-quality one”

This does exist. Advisors always have an incentive to appear better than they are.

3. “Sellers have no credible disclosure technology (sellers with a great car have no way to disclose this credibly to buyers)”

This is another failure. Advisors do have ways to demonstrate their expertise and client service prior to a transaction.

4. “Either a continuum of seller qualities exists or the average seller type is sufficiently low (buyers are sufficiently pessimistic about the seller’s quality)

A continuum definitely exists. It’s arguable whether buyers are sufficiently pessimistic about advisor quality, but this doesn’t seem to be a big enough divergence from the assumption to say it is untrue.

5. “Deficiency of effective public quality assurances (by reputation or regulation and/or of effective guarantees/warranties)”

Again, the effectiveness of regulation is arguable, but regardless, the failures of (1) and (3) are sufficient to make this application to the advisor market inappropriate.

This isn’t a licensing issue. It’s an education standard issue. The licensing is mostly a waste of time. Who remembers all the different acts of 1936 or 1986, and what value do they really have? This licensing should be a small part of getting into the business. There is no education or knowledge requirement, and the age old argument that this will lead to higher costs for the customer “we are trying to protect” is garbage and mostly job justification. If you really want to protect your customer, like Michael said, you have to know what you are doing, rather than just selling. You can be a fiduciary and responsible, and try to do what’s in your clients best interest, but that doesn’t mean what you are doing is protecting your client if you don’t have the education, training and experience.

Anyone who argues against setting education and training requirements is a salesperson worrying about their job, not protecting their clients.

Doctors could use the same arguments and do away with medical school

Michael,

Very few advisors have sufficient support outside of their own RIA to meet the fundamental threshold for fiduciary standing as required by statute of those who render individualized advice. Broker/dealers assure their “brokers” do not render advice by virtue of their FINRA and SIFMA condoned internal compliance protocol, so to avoid fiduciary liability. Custodians, as vendors do not want to assume fiduciary liability, thus fear their of supporting fiduciary duty would be deemed prescriptive which would indeed trigger fiduciary liability. To date only our largest RIA are acting as fiduciaries and afford affiliated advisor professional standing for the life of their clients and their heirs as required by statute. The industry is at the inflection point where huge market share is in play for firms that afford large scale institutionalIzed support for expert authenticated fiduciary standing. For those that are curious about cost, expert fiduciary standing is less expensive than commission sales which eats 15% of gross industry revenues (equivalent to most firms 15-20% profit margins) in compliance cost to assure the broker renders no advice.

SCW

Stephen Winks

“To date only our largest RIA are acting as fiduciaries and afford affiliated advisor professional standing for the life of their clients and their heirs as required by statute”

Where are you getting this info from? What constitutes the “largest”? What do you mean by “afford affiliated advisor professional standing”? Do you mean that somehow the RIA is paying for some sort of fiduciary training / adherence? Please explain for those not exactly familiar with what you’re trying to say.

I don’t think you’re saying only large RIAs are acting as fiduciaries- at least I hope not. If you are saying only large RIAs are fiduciaries, you’re way off base.

It would certainly help if ordinary savers with money to invest could actually see what a so-called financial advisOr’s/advisEr’s educational background was. Does (s)he have a high school diploma? Does (s)he have a college degree? If so, in what, child development? Is there someplace where a person can access this information? FINRA doesn’t list it which makes me think that there are a lot of brokers who have little to no education. Yikes! and we savers are supposed to entrust our lifelong, hard-earned, irreplaceable savings to someone that might possibly have no basic education–reading, writing and arithmetic? Might these be the guys and gals who lack a moral compass?

There is no education requirement, not even a high school degree, to get a job in any of the 3 areas mentioned.

The sad thing is most clients think their ‘advisor’, most of whom are salespeople at the big brokerage firms, is awesome, smart and ‘watching my portfolio’ all the time. Not just the morning of the annual review, which is more common.

It’s almost analogous to the Republican primary. Donald Trump is exposing how politicians get ‘paid’, which means elected. I’m amazed that it took until Trump for the average voter to figure that out. It’s not because they can or will implement the best policies for their clients ( constituents), it’s because they raise the most money (commissions) and get to shape and sell themselves in the media. We think we’re getting a politician who is doing what’s best for us, but in reality he’s doing what’s best for himself (and those who put him into office with big donations). We then wonder why we don’t get the results we were promised during the election cycle.

Same for the salesmen in this article. We think we are getting experts in their field, experts in markets and economics and all money related matters. In reality, as the article says, we’re getting salespeople with no formal education or expertise other than rules and regulation training, as well as sales training from their companies. As a matter of fact, most companies have extensive training programs, and it is all sales related. Many of these companies even encourage, and sometimes pay for, their salespeople to get the CFP certification for credibility. But even with this, they are still driven and measured by commissions, and ranked by their companies for year end honors and trips. All based on commissions generated. And, they have quotas to meet to keep their jobs.

It’s going to be a long time before education requirements will be in place for this industry. One big reason is the Pacs and lobbyists who work for the industry and these financial companies, who will influence the politicians to defeat proposals for this type of reform.

I think the industry wants you guys to keep talking about this until they can replace you with machines…

If the licensing requirements are considered too easy for financial planning you must not be very familiar with the testing industry. Realtors and loan officers take similar exams for huge decisions regarding your life and your home purchase or mortgage is of equal importance. It is important to realize that exams are designed to make sure the person has a fundamental knowledge of the industry. The expectations you want would require an apprenticeship similar to what’s required for licensed appraiser. The standards are not too easy. You

want a requirement that is not realistic you and are not familiar with traditional testing for professional practice. Your idea is not sustainable.

You realize the testing standards being discussed here are ALREADY fully implemented in varying forms for doctors, lawyers, accountants, and many other professionals?

I’m not quite sure how the idea can be “not realistic” and “not sustainable” when it’s already a realistic, sustainable practice in a wide range of other recognized professions…

– Michael

I think one element of this problem is that many firms are still based on an “eat what you kill” mentality. Not in all firms, but in many, new associates aren’t paid, or are paid small stipends that barely allow them to support themselves. In many cases, if they are unable to quickly (within a year or two) amass a client base, then they are pushed out of the industry. And if they do manage to bring in some new clients and their earned fees go up, their stipend goes down, resulting in a personal income flatline for many young associates. This isn’t exactly a scenario someone would seek out extensive educational training for. And if they were to arrive on day one with a masters in Financial Planning and prepared to sit for the CFP exam, I doubt many firms today would be willing to pay them a salary on par with their medical resident peers without the expectation that they immediately begin to bring in business. Not to mention those residents are taking a small salary with the expectation that a significant increase in pay awaits them. I believe that as long as our industry’s model for hiring new advisors offers such weak initial incentives, the intelligent graduates will continue to look elsewhere, leaving the industry hollowed out, clinging to a handful of truly competent advisors like Michael.

Making it more difficult to enter the profession also requires an incentive for new professionals to accept the challenge.

This is the real problem.

I think I will call myself a “policeman” because I stopped a fight between two young boys. Then I think I will call myself a “surgeon” because I bandaged a scrape that one of the boys got on his arm. Then I think I will call myself a “psychologist” because I helped the boys understand why this was wrong. Then I think I will call myself a “lawyer” because I had to discuss the situation with each of the boy’s parents. Then I think I will call myself a “financial planner” because I sold one of the parents a life insurance policy.

In a free country, you should be able to call yourself whatever you please. And others are free to not take you seriously for it.

Licensing is not necessary. What is necessary is good sense, continual education, solid conventions and voluntary social networks to help people find their way.

Whatever test the government created will be mostly useless, irrelevant or misleading from day 1.

Caveat emptor. That’s the reality of life. And it doesn’t go away when laws are passed.

If you buy that politicians are “protecting” you with these laws, I’d suggest that you may need to internalize that phrase and remember what it means.

Justin,

While I believe we are of the same thought in that we have a country with too large of a government with too many laws, and full of selfish emperors I might add, I am very glad that there are educational and ethical requirements in most professions.

And while I also believe there is too much regulation, living without any type of law is anarchy. Imagine driving on the highway where there are no speed limits. Or if speed limits or reckless driving were not enforced. I think most people prefer some controls versus none.

Throwing the baby out with the bath water is dangerous thinking. What I, and others I respect have found is that too much, or not enough, of whatever it be, laws, regulation, food, exercise, sleep, etc., is at the least undesirable, but often down right dangerous. Having a reasonable moderation range is the key.

I ask you and any other readers to test the theory of a moderation range. I think they will find it holds true in almost anything.

I wish you the best in whatever endeavor and profession you have chosen.

Thanks Rob. I do agree that standards are important. My only recommendation is that they be handled and developed by competing voluntary institutions, rather than by a forcible state monopoly. The approach I am recommending is actually the way it has been properly handled for much of our history since the enlightenment.

At the end of the day, there is no one “right” way to invest. And, discovering “better” ways to invest requires experimentation and competition. The same is true in all fields of practice.

Nowhere here have I advocated for anarchy or for lawlessness. Again, I would offer that it is very important indeed that people have means of legal recourse for those rare cases of negligence or fraud that do occur. That is a just and proper role for government.

Handling negligence and fraud however, is best handled not by a top-down state monopoly on “regulation”, but rather by government providing a system of courts for settling criminal cases and civil disputes.

This is what it means to live in a free society: Each person is free to do as they pleases so long as they are not harming others by committing fraud, breaching their agreements through negligence, or otherwise infringing on the equal rights and freedoms of others.

That is the appropriate role of government. Its proper role is not to to micromanage any profession or to impose a forcible “one-size-fits-all” monopoly on regulation. That part meant to be handled by free people, experimenting and competing to find the best ways to collaborate with one another.

I hope that makes sense.

Hi Justin,

Thank you for your clarification. Our government has gone from serving the people to thinking they know what is best for the people. And we are forced to pay their idea of fair taxation. Anecdotally, I have found it alarming that we are country that thinks the rich are liable for paying more taxes, as a percentage of their income. Really? Many wealthy business owners are innovators, and create many jobs for those that neither have the skills nor desire to build their own business.

Certainly there are good and bad business people, just as there are in any profession. But as a society many assume that the wealthy got there because of something they did unfairly. Nobody seems to say anything about the risks business owners take, or the sacrifices they made to make their company profitable.

I have digressed, I know. But as you can probably tell, you and I are both tired of the tyranny. Who is checking the checkers, right? I would hope others will see the wisdom and fairness that Friedman professed.

And I agree that the government should not be micromanaging. It is simply impossible to effectively manage all they want to manage. I do not see a Solomon anywhere, and even he would be severely challenged to oversee so much detail.

I think our biggest difference is that we differ on our trust in mankind. I see man (and woman) primarily acting in their own self interests, even if it us done unfairly or unjustly to another. I am fortunate to know a number of people who do not function this way, but sadly I believe this is a small percentage. I do not trust human nature, and but of course the challenge is also with those making the laws: Are they acting in their own self interests?

It is difficult to draw the line where man is given freedom to do what he chooses, but also take proactive measures to make sure his nature does not take advantage of, hurt or even kill another. I think we both agree on freedom, but I think I have less faith in mankind than you do.

Thought provoking as always. I agree that there should be some academic standard for providing financial advice, though the devil is in the details as to what that standard should be. Perhaps there might be multiple minimum standards, such as attainment of the CFP marks, undergraduate degree in finance, economics, or accounting, MBA, CFA, etc.

Ironically, I was turned off by the CFP program in the mid-1990s because I felt that it was too biased toward the sale of insurance products. For its part, prior to 2006, a college degree was not a pre-requisite for the CFP exam. Even today, it is my understanding that no prior academic background in finance or econ is required. For the record, I have great respect for my friends in the CFP community and do not dispute their qualifications. Just making a point. I am also not sure there is any correlation between academic qualifications and ethics.

Lastly, were such a standard to be implemented, what would be the impact on existing advisors? Similarly, the CFP Board has done much to distance the financial planning profession from its insurance sales-oriented roots, but what of the legions of CFPs who attained the marks long before the standards became so rigorous?

An advisor’s/planner’s client is going to own a collection of products. Of course, this is not the case with the clients of attorneys and accountants. To varying degrees, any form of investment advice is a form of product distribution. And in all 3 approaches discussed in Michael’s article there is an important common element: the individual advisor bears the greatest responsibility and liability. The industry is governed through product “disclosure,” not product “efficacy.” By design, liability issues are born not by product manufacturers, but by the individuals making the recommendation. The securities industry is unique: it is product centric without the burden of being subject to product liability laws. Imagine if the automobile industry operated like this.

Well stated!

Loved all the discussion. The difference between Financial Planning and all the other licensed professions is the huge differential between need and affordability. There are mechanisms for everyone to get the same $15 haircut or $300 doctor visit, and then pay for premium services if desired. There are limited processes for everyone to get a financial plan at an affordable price despite the great need. As a result, there are very few paths for individuals with a passion for true financial planning to make it a career without the support of product sales and their potentially negative impact relative to Fiduciary Standards. High Net Worth individuals have the resources and networks to find the solutions that most do not. We need some significant disruption in this industry, but it should not be driven by more regulation! That will only slow the needed change in business models.

So the trades and professions with structured entry points have accessible mechanisms for everyone, while our grossly low standards can’t figure out how to provide the same breadth of services.

Not a coincidence… there’s a reason why professions have established minimum requirements. It’s absolutely essential for creating the consumer trust necessary to broaden services and make them more affordable for all. Otherwise, low trust and high acquisition costs lead quality players to concentrate at the high end of the market, and low-quality players dominate and abuse the rest. :/

– Michael

Couldn’t disagree more (a rarity for me). Anchoring on hairstylists or on physicians is bad logic. Licensing a hairstylist is rediculous. How many deaths or severe injuries have they caused? One bad haircut and the market will take care of them in short order. Meanwhile, medical negligence is the third leading cause of death in the U.S. (just behind heart disease and cancer) and rife with conflicts of interest. There is a clear overconfidence of licensing and no amount of licensing can keep out the bad apples. Let the merits of financial planning stand on their own. Going through some of the CFP coursework right now has me LESS confident in my peers’ ability to deliver knowledgeable advice. However, I think it serves to give the advisor more confidence in themselves (arguably too much confidence). Any licensing system imposed or otherwise created for an industry is mostly a disguised way of reducing competition by creating barriers to entry. Yes, let the buyer beware. And let advisors prove themselves on their own merits, not the arbitrary standards of yet one more bureaucracy.

The question then becomes, how do we change the standards? Set up a similar to that of Lawyers or Doctors to demonstrate both knowledge and experience before we let someone provide advice on a person’s life savings?

In a free country, you should be able to call yourself whatever you please. And others are free to not take you seriously for it. Tort can handle the rest.

Licensing is not necessary. That’s what’s better known as “protection” of an industry, and a very good case can be made against it for hairdressers and financial advice-givers and just about everyone else.

What is necessary is good sense, continual education, solid conventions and voluntary social networks to help people find their way. (Plus, courts of common law, where cases can be brought in Rafe cases of negligence or fraud.)

One might reasonably draw the line at doctors and drivers and others who pose a real danger to life and limb, but even then a strong case can be made to the contrary.

(Sometimes 21st century history looks to be an ongoing process of society catching up to arguments that Milton Friedman made 50 years ago 🙂

Regardless, whatever test the government creates along these lines will be mostly useless, largely irrelevant, and often grossly misleading from day 1, just as they are in most industries. (Even medical licensing leads to sustaining truly backward practices and advice for far longer than they might in a freer market environment.)

Caveat emptor. That’s the reality of life. And it doesn’t go away when laws are passed.

If you buy that politicians are “protecting” you with these laws, I’d suggest that you may need to internalize that phrase and remember what it means.

A better approach is to crack down on the people who commit financial crimes, and allow people who are entering into the field to start regardless of their current financial well being. I’ve been looking at this for a long time and I have found that people who actually cheat their clients and commit fraud are able to keep practicing. Bernie Madoff got a lot of press, but he was merely a spectacle. The law allows plans to lock you in so you cannot move your money out if you are getting a low return. Locking people into these low yield plans costs individuals millions of dollars. (I’m a trained economist, I see no difference between money spent and money not earned) If an advisor is doing a good job they will not need to lock their clients money into their firms because most of their clients won’t leave. Cracking down on other rampant abusive practices which are 100% legal would go a long way towards bankrupting corrupt advisors and allowing new, fresh, compassionate, and honest advisors into the field. We currently do the opposite where it is hard for young college grads to enter with very expensive licensing fees, and very few people who actually harm their clients lose their licenses.

I don’t the licensing and other requirements to become a financial advisor are too easy. It would help if you worked hard to get to a point where people will come to you for financial advice.