By reducing the cash conversion cycle—a key metric monitoring the length of time between when a company buys a product from a supplier and the collection of payments from customers for that product—companies can increase profitability significantly. The cash conversion cycle measures how fast a company can convert cash on hand into even more cash on hand. The longer it takes a company to turn raw materials into sales revenues, the longer that company’s working capital is tied up and can’t be utilized to grow its business and increase profits.

Smart, efficient management of working capital can potentially free up cash for other uses that can build shareholder value. The extra cash can also reduce the company’s reliance on debt or other forms of external financing while, at the same time, help to strengthen the balance sheet and enhance operational performance. And, depending on the company’s plans for growth, the extra cash can also be used to build shareholder value through mergers and acquisitions. Investors usually take this as a good sign since working capital is often considered a proxy for the strength of how well a company is run.

THE CHALLENGES

Working capital is a simple concept because it’s all about freeing up the company’s cash. Unfortunately, many organizations face serious internal challenges that can interfere with their ability to do so. As they’ve discovered, it’s one thing to recognize the need for working capital improvement and quite another to understand what steps to take to improve cash flow.

To put this into perspective, here are some current challenges to improving working capital:

Limited access to needed information. Many companies lack the real-time data and metrics needed to evaluate the effectiveness of their working capital strategy and improve it.

Lack of formal structure. It can be difficult to sustain the working capital improvement effort without a formal structure. Few companies have a formal improvement program with clear ownership across the organization, or, worse, they lack the tools and the capabilities to implement such a program.

Too many stakeholders and perspectives. The widely distributed nature of working capital can make it difficult to implement a working capital improvement program. Each stakeholder is likely to have a different perspective on how to enhance working capital and the relevant priorities.

Time constraints. Organizations often struggle to focus on improving working capital because of other priorities competing for their attention.

Finance leaders are in the best position to address these challenges. As guardians of cash flow, they’re the professionals who are often positioned to do the strategic visioning and lead a working capital improvement effort.

CASH MANAGEMENT CULTURE

As financial professionals, the ability to establish the infrastructure to support working capital improvements is in your tool belt. With your training and experience, you can provide the leadership needed to build a cash management culture that includes a formal working capital strategy, appropriate drivers and metrics, and clearly communicated policies across the organization. The result will be enhanced accounts receivable, accounts payable, and inventory management processes, which will lead to working capital improvement.

An effective program should start with a “tone at the top” directive from the board of directors, CEO, and CFO. Senior management should make it clear that improved working capital is linked to both business and individual performance. Because working capital touches so many different parts of an organization, finance leaders should collaborate with other leaders within the business to share the goal of improving working capital and adding the program into their systems, analytics, and performance metrics.

There are levers throughout an organization that can help drive working capital improvements, such as managing inventory more efficiently, embedding specific working capital metrics in forecasting, and improving the management of accounts receivable and accounts payable. Metrics should be built into the improvement program’s goals and used as a consistent feedback mechanism so that finance and treasury can monitor the program’s effectiveness and impact. Additional measures can be used to determine the capital required to fund manufacturing processes or to create dashboards that provide daily views of metrics that impact cash flow and working capital over time.

How do you sustain working capital improvements? There should be company-wide incentives that foster management focus and change, as well as real links to business performance and overall compensation. You should also have the flexibility to adjust for external factors that may adversely affect working capital, such as changes in the global economy, the limited availability of financing resources, and suppliers who are unable to meet company needs because of their own internal capacity challenges.

Of course, approaches to improving working capital management will vary depending on the industry and the company’s situation, but they should have three overall objectives: (1) reduce inventory, (2) speed up collection of receivables, and (3) reconsider payment terms.

CROSS-FUNCTIONAL APPROACH

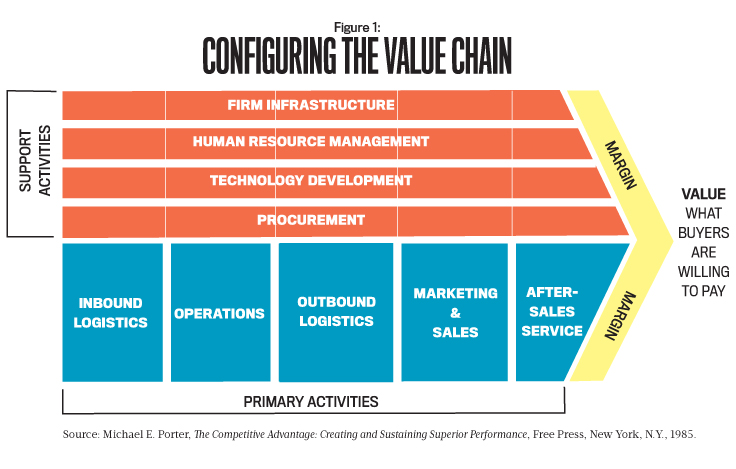

Cash flow management is a cross-functional organizational concern. To gain an enterprise-wide view of cash management, it’s important to track sources and uses of cash by both type and location. It also means engaging the sales, procurement, and operations functions in a meaningful way. All this takes place along the value chain, which is a set of activities that a company operating in a specific industry performs in order to deliver a valuable product or service for the market. Michael Porter first described and popularized the concept in his 1985 best seller, Competitive Advantage: Creating and Sustaining Superior Performance. See Figure 1 for his value chain example.

Companies that use a cross-functional approach to working capital management don’t wait for problems to occur; they anticipate them and, when necessary, make quick adjustments. By analyzing each component of working capital along the value chain and streamlining key processes, organizations can identify and remove the obstacles that slow cash flow.

Too much working capital usually means that too much money is tied up in accounts receivable and inventory. The typical knee-jerk reaction to this problem is to aggressively collect receivables, suppress payments to suppliers, and cut inventory across the board. Unfortunately, this approach addresses only the symptoms of working capital problems, not the root causes.

A more effective approach is to reassess and refine key processes across the value chain, processes that can lead to significant reductions in working capital. Companies must analyze the entire value chain from product design to manufacturing, sales, and customer service to identify hidden interdependencies and maximize savings. The key is to uncover the underlying causes of excess working capital across the entire value chain.

By refining end-to-end processes, companies can reduce buffer stock, decrease restock times from internal and external suppliers, and improve cash collection and payment cycles.

Best practices in working capital management that include new processes, expertise, and supporting technology work together to reduce working capital requirements across the three primary drivers of inventory, accounts payable, and accounts receivable. Companies need to manage all three simultaneously across the value chain to free up cash to fund strategic investments while delivering improved results to shareholders. It’s actually a rather simple formula: Strong disciplines in working capital management lead to strong disciplines in operations, which lead to significant gains in resource productivity and profits.

IMPACT ON CUSTOMERS, SUPPLIERS, AND PARTNERS

Companies must look for ways to simplify processes and eliminate costs, keeping in mind how these changes may affect other areas in the value chain. Improving working capital management can affect customers, suppliers, and partners. For instance, lowering the level of spare repair parts or reducing product customization could lead to a major reduction in inventory. But how would these measures affect service quality, marketing strategies, or other aspects of the business?

Building strong, transparent relationships with customers and suppliers is the key to flexible working capital policies that are mutually beneficial and that can be adapted to business cycles. Having strong external relationships means a company has room to negotiate new agreements with customers or suppliers that are mutually beneficial to everyone.

Now let’s take a deeper dive into the three critical areas mentioned earlier—inventory, accounts payable, and accounts receivable.

INVENTORY

Excess inventory is one of the most overlooked sources of cash, frequently accounting for most of the savings from improved working capital management. By streamlining cross-enterprise processes, as well as processes involving suppliers and customers, companies can minimize inventory throughout the value chain. For example, high inventory costs could result from problems with an internal production process or a supplier’s delivery lead times. They could also result from a needlessly complex product design, a problem that the engineering group may be able to resolve.

Companies often can achieve substantial gains by reducing raw materials and work-in-process inventories through product design and process improvements, improvements that can lead to smaller safety stocks, time buffers, and batch sizes. This requires a thorough analysis of customer demand patterns, production throughput time and variability, and supplier lead times. These improvements can greatly decrease raw-material and work-in-process inventories, but they require end-to-end process improvements across the value chain from the supplier to the customers.

ACCOUNTS PAYABLE

Does your organization have problems with accounts payable? This could be the result of making payments earlier than necessary or from failing to negotiate payment terms with suppliers. Fast-paying companies are at one end of the spectrum; at the other end are companies that lean on the trade and use unpaid invoices as a source of financing. Between these two extremes is a more effective, integrated approach to payment renegotiation that takes into account all aspects of the customer-supplier relationship from price and payment terms to delivery time frames and product-acceptance conditions.

If you haven’t done so, your company should benchmark terms and conditions against industry best practices and eliminate early payments, except when attractive discounts are offered. When renegotiating payment terms, consider the length of your relationship with your suppliers as well as competitive loyalties. In addition, linking suppliers’ payment terms to their performance in areas such as delivery accuracy, complaint ratios, and order lead times can improve underlying processes and reduce working capital overall.

ACCOUNTS RECEIVABLE

High levels of due and overdue receivables could be a result of delayed payment reminders and late dunning, but they could also result from problems with product quality or a failure to meet customer expectations. By aligning service levels with customer needs in areas such as order lead times and delivery schedules—and tying those service levels to payment terms—companies can improve cash flow and customer service at the same time.

But a word of caution: The goal of shortening customers’ payment terms must be balanced against the risk of jeopardizing the relationship. Companies should always seek a fair, mutually beneficial, and nonconfrontational solution.

Some companies, particularly project-based businesses and manufacturers of large, costly products with lengthy production cycles, have cash flow problems caused by a mismatch in the timing between incurred costs and receipt of customer payments (the construction industry is a perfect example). One way to ensure a steadier flow of cash is to better align incurred costs with customer payments by asking for a down payment and setting up a series of staggered payments to ensure that most receivables have been collected by the time of delivery.

MEASURING AND MONITORING

Many companies don’t systematically track or report granular data on working capital. This is a challenge because getting data from multiple legacy systems into a consistent and usable format can be tedious and time-consuming, making it difficult to execute strategy on an ongoing basis.

Data collection should be built into the company’s core IT processes, which can draw on a single integrated system to automate the process. Using ERP systems, organizations are able to disseminate information faster than they would be able to by using more conventional means, such as written reports. The accumulation and use of data are qualities of an effective working capital management system.

Metrics also have an important place in your system as long as they’re aligned with overall company strategy and communicated across the organization. Metrics may change year to year as the strategy changes, so make sure that yours are specific to your industry and company.

Keep the number of metrics manageable so that you and other financial leaders in your company can communicate them clearly and employees know what to focus on. Five or fewer key metrics are plenty. They should be monitored at all levels within the organization from the executive offices to the employee break room. Posted metrics help keep everyone focused on achieving improvements.

As you can see from this discussion, the reasons to consider a system of working capital improvements are compelling. By analyzing each component of working capital along the value chain, companies can identify and remove the obstacles that slow cash flow. Done right, working capital management generates more cash for growth along with streamlined processes and lower costs. In addition, boards understand that efficient management of working capital can potentially free up cash for other uses that can build shareholder value.

For finance leaders such as you, who are charged with growth and are determined to steer strategy, effective working capital management can provide the cash your organization needs to succeed now and in the future.

SIDEBAR: Working Capital Management: Implications for Small Companies

Working capital management is especially important for small companies with limited financial resources. They may have trouble accessing working capital through debt and equity markets because smaller companie are considered riskier, making it harder for them to secure loans. In addition, small companies are generally charged higher interest rates compared to large companies.

Many small companies are seasonal or cyclical businesses that often require working capital to meet their financial obligations during the off-season. For example, an indoor waterpark or a restaurant with a lot of outdoor seating may do significantly more business during the summer months, resulting in large payouts at the end of the tourist season. Nevertheless, the company must have enough working capital to buy inventory and cover payroll during the off-season, when revenues are lower.

If you work for a small company, a cash flow projection can help you manage your cash so the company can pay its bills on time. It’s a great tool for setting sales goals and for planning for expenses to support those sales. As your business grows, it can also help you plan for a large expenditure, such as an equipment purchase or a move to a new location, so that you have the cash on hand when you need it.

SIDEBAR: Working Capital Management: Best Practices Checklist

An organization’s working capital management improvement program should include:

- Aligning overall operational processes with stated strategic intent

- Engaging executive-level support for, and involvement in, working capital improvement

- Centralizing and standardizing financial transaction processing to drive maximum efficiency and to draw meaningful insights from underlying data

- Taking a cross-functional approach to working capital accountability and continuous improvement of receivables and payables processes

- Using data from an enterprise resource planning (ERP) system to inform daily credit and collection activities

- Conducting real-time analysis of cash flow drivers to ensure reliable forecasts and optimize spare cash

- Analyzing, measuring, and advising operating units on how to increase the return on working capital

- Designing custom measures of working capital management that are relevant to operating units’ business models

- Applying quality and productivity tools to process improvement efforts in finance

- Leveraging change-management principles and practices in finance

- Identifying and resolving data discrepancies on the front end of the process

- Managing working capital risk

- Offering self-service to drive efficiency

- Conducting transactions electronically whenever possible and working with vendors so they can do the same