Abstract

This paper proposes a model to study how conditional lending and immediate liquidity provision affect incentives for fiscal adjustment in a country facing the risk of sovereign default. Conditional lending provides explicit incentives for fiscal adjustment but immediate liquidity provision is more effective in reducing liquidation costs. For some parameters, immediate liquidity provision induces fiscal adjustment and debt repayment, while conditional lending does not (and vice-versa). Incentives for fiscal adjustment are concave in the fraction of lending provided under conditionalities. A large cost of tight fiscal policy shifts the balance toward immediate liquidity provision.

Similar content being viewed by others

Notes

-

A description of all types of credit lines granted by the IMF can be found at www.imf.org.

-

In most of the literature, creditors are risk neutral, so the domestic economy can always borrow at the actuarially fair price. Lizarazo (2013) considers the case with risk averse lenders, which generates a risk premium in the model.

-

See Panizza et al. (2009) for a survey of this literature. The costs of sovereign default might stem from a reduction in international trade, perhaps owing to trade sanctions (see, e.g., Rose (2005) and Martinez and Sandleris (2011); reputational costs that affect access to finance or the country’s position when negotiating with other nations (see, e.g., Tomz (2007) and Fuentes and Saravia (2010); domestic problems caused by the redistribution of wealth resulting from the sovereign default (see, e.g., Broner and Ventura (2011); among others.

-

Section 3.3 considers the case where taxes have a negative effect on output.

-

Caballero and Krishnamurthy (2001) model liquidity needs in a similar way.

-

Mishkin (1999) adds that “an important historical feature of successful lender-of-last-resort operations, is that the faster the lending is done, the lower is the amount that actually has to be lent.”

-

There is no uncertainty in the model, so more detailed IMF preferences would not affect the results. In equilibrium, the IMF knows whether the country will choose to repay its debts or not (conditional on the IMF’s own choices). We thus assume that the IMF wants to avoid a debt default, and then study whether immediate liquidity provision or conditional lending are more effective in providing incentives for fiscal adjustment and repayment.

-

If \(D\) happened to be larger than \(\Gamma \), then the government would choose to default, and there is nothing that the IMF could do about it. This is a case where it is never optimal to repay the contracted amount of debt.

-

Fafchamps (1996) analyzes conditionalities that increase the cost of defaulting (\(\Gamma \) in this model). For example, trade openness might increase the potential costs from trade sanctions. In that kind of model, ex-post conditionalities might be an optimal response to larger debt, but fiscal conditionalities play a different role.

-

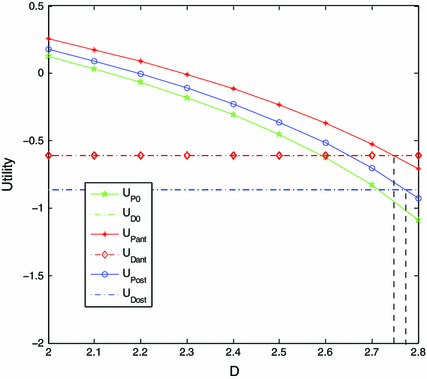

The remaining parameters are: \(Y=7.68\), \(\ell _{2}=1.4\), \(\phi _{1}=2.56\), \(\phi _{2}=1.6\) and \(\Gamma =3\).

Fig. 1

Conditional lending provides more incentives for adjustment

-

For \(\ell _{1}=0.997\), incentives for repayment with \(\lambda =0\) and \(\lambda =1\) are exactly the same, in the sense that the respective thresholds for the level of debt \(D\) consistent with repayment coincide.

-

In fact, a capital account position dominated by private flows is one of the criteria mentioned by the IMF for access to a flexible credit line: http://www.imf.org/external/np/exr/faq/facfaqs.htm#q6.

References

Bird, G. (2007). The IMF: A Bird’s eye view of its role and operation. Journal of Economic Surveys, 21, 683–745.

Broner, F., & Ventura, J. (2011). Globalization and risk sharing. Review of Economic Studies, 78, 49–82.

Caballero, R., & Krishnamurthy, A. (2001). International and domestic collateral constraints in a model of emerging market crises. Journal of Monetary Economics, 48, 513–548.

Calvo, G. (1998). Capital flows and capital-market crises: The simple economics of sudden stops. Journal of Applied Economics, 1, 35–54.

Collier, P., Guillaumont, P., Guillaumont, S., & Gunning, J. W. (1997). Redesigning conditionality? World Development, 25, 1399–1407.

Conway, P. (2006). The International Monetary Fund in a time of crisis: A review of Stanley Fischer’s IMF Essays from a Time of Crisis. Journal of Economic Literature, 44, 115–144.

Corsetti, G., Guimaraes, B., & Roubini, N. (2006). International lending of last resort and moral hazard: A model of IMF’s catalytic finance. Journal of Monetary Economics, 53, 441–471.

Cuadra, G., Sanchez, J. M., & Sapriza, H. (2010). Fiscal policy and default risk in emerging markets. Review of Economic Dynamics, 13, 452–469.

Dreher, A. (2009). IMF conditionality: Theory and evidence. Public Choice, 141, 233–267.

Dreher, A., & Jensen, N. (2007). Independent actor or agent? An Empirical Analysis of the Impact of US International Monetary Fund Conditions. Journal of Law and Economics, 50, 105–124.

Easterly, W. (2005). What did structural adjustment adjust? Policies and growth with repeated IMF and World Bank adjustment loans. Journal of Development Economics, 76, 1–22.

Eaton, J., & Gersovitz, M. (1981). Debt with potential repudiation: Theoretical and empirical analysis. Review of Economic Studies, 48, 289–309.

Fafchamps, M. (1996). Sovereign debt, structural adjustment, and conditionality. Journal of Development Economics, 50, 313–335.

Fischer, S. (1999). On the Need for an International Lender of Last Resort. Journal of Economic Perspectives, 13, 85–104.

Fischer, S. (2004). IMF essays from a time of crisis: The international financial system, stabilization and development. Cambridge, MA: MIT Press.

Fuentes, M., & Saravia, D. (2010). Sovereign defaulters: Do international capital markets punish them? Journal of Development Economics, 91, 336–347.

Gonçalves, C. E., & Guimaraes, B. (2013). Sovereign default risk and commitment for fiscal adjustment. Working Paper.

Lizarazo, S. (2013). Default risk and risk averse international investors. Journal of International Economics, 89, 317–330.

Martinez, J., & Sandleris, G. (2011). Is it punishment? Sovereign defaults and the decline in trade. Journal of International Money and Finance, 30, 909–930.

Mishkin, F. (1999). Lessons from the Asian crisis. Journal of International Money and Finance, 18, 709–723.

Morris, S., & Shin, H. (2006). Catalytic finance: When does it work? Journal of International Economics, 70, 161–177.

Nooruddin, I., & Simmons, J. W. (2006). The politics of hard choices: IMF programs and government spending. International Organization, 60, 1001–1033.

Panizza, U., Sturzenegger, F., & Zettelmeyer, J. (2009). The economics and law of sovereign debt and default. Journal of Economic Literature, 47, 651–698.

Rochet, J.-C., & Vives, X. (2004). Coordination failures and the lender of last resort: Was Bagehot right after all? Journal of the European Economic Association, 2, 1116–1147.

Rose, A. (2005). One reason countries pay their debts: Renegotiation and international trade. Journal of Development Economics, 77, 189–206.

Stone, R. (2008). The scope of IMF conditionality. International Organization, 62, 589–620.

Tomz, M. (2007). Reputation and international cooperation. Princeton: Princeton University Press.

Acknowledgments

We thank the editor Andreas Haufler, Enlinson Mattos, Mauro Rodrigues Jr, André Portela Souza, two anonymous referees and seminar participants at the ANPEC Meeting 2013 (Iguaçu) and the Sao Paulo School of Economics – FGV for helpful comments. Bernardo Guimaraes gratefully acknowledges financial support from CNPq.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Guimaraes, B., Iazdi, O. IMF conditionalities, liquidity provision, and incentives for fiscal adjustment. Int Tax Public Finance 22, 705–722 (2015). https://doi.org/10.1007/s10797-014-9329-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-014-9329-9