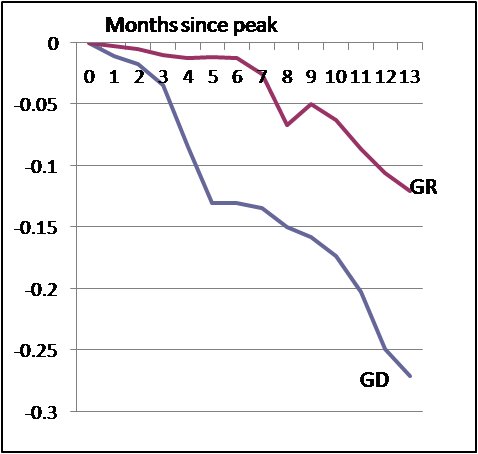

Reading this article about the global manufacturing plunge, I wondered: how does the current slump stack up against the early stages of the Great Depression? The US has consistent industrial production data back to 1919, so it’s a fairly straightforward exercise. Below is the change in industrial production, measured in logs, from the previous peak in 1929-30 and 2007-9.

At first, the current recession didn’t hit industrial production all that hard. But the pace accelerated dramatically last fall, so that at this point we’re sort of experiencing half a Great Depression. That’s pretty bad.

Clarification: Those are natural logs — sorry, economists use them so frequently I forgot to explain. So basically multiply by 100 to get the percent change.

Comments are no longer being accepted.